This week in incredibly bad auditing, we have Terry L. Johnson of Casselberry, Florida. And if you like devouring stories of grossly deficient audits and Florida men doing ridiculous things, then this should satisfy your appetite.

Let me just tell you first that some form of the words "so deficient that they amounted to no audits at all" appear four times in the SEC Order. I'm not joking! Paragraphs 2, 21, 65 and 81. But when you learn how Johnson landed this work, the rest becomes far less surprising:

Okay, so we have a guy with no prior experience as a partner on registered entities acquiring 18 clients from his previous firm that was censured and barred by the PCAOB. That sounds like the perfect recipe for something like this:

Okay, so we have a guy with no prior experience as a partner on registered entities acquiring 18 clients from his previous firm that was censured and barred by the PCAOB. That sounds like the perfect recipe for something like this:

Johnson was engaged to perform a re-audit of the December 31, 2012 year-end financial statements of six audit clients, including, ADM, Boreal, Legendary, Monster, Puissant, and UMED, as a result of the PCAOB revoking the registration of the predecessor auditor. Johnson was required to take full responsibility for the 2012 audits and perform his own audit work that provided a basis for his opinion on the financial statements. Johnson, however, relied on the predecessor auditor’s audit work to afford a basis for his 2012 audit opinions, without performing an independent audit.

And this:

[V]irtually no work papers existed for the Boreal and Puissant audits. The majority of work papers for the Monster audit only contained a notation from Johnson indicating that he “traced to w/p in prior auditor file, reviewed procedures.”

And this:

For the audit of Primco, for example, Johnson had no copy of the issuer’s Form 10-K (or subsequent amended 10-Ks) in his workpapers. Primco subsequently restated its Form 10-K because it later came to Johnson’s attention that the issuer “inadvertently” included among other things, approximately $1,496,000 in assets on the balance sheet that should not have been recorded in the company’s books and records. Significantly, as a result of the restatement, certain amounts reflected in Primco’s original tax footnote should have changed in the restated filing but were not. Johnson, however, did not review the tax footnote.

Then there's this beauty:

Further, for the audits of Monster and Boreal, for example, the work papers included a printout of the issuers’ filings with a header containing the SEC EDGAR internet address, demonstrating that that the filings were printed from the SEC EDGAR website and inserted in the work papers after they were filed with the Commission.

By now you might be thinking, "All we're missing are some back-dated and fraudulent workpapers." Don't worry!

In a September 23, 2014 email from Johnson to the CEO of Puissant, following the staff’s request for documents, Johnson sent a“management inquiries” work paper and a “SAS 99 fraud questionnaire” work paper—critical parts of an audit—and asked “can you get these back to me as soon as possible.” Puissant’s CEO, on that same day, responded “signed documents…” and attached completed copies of the “management inquiries” and “SAS 99 fraud questionnaire” work papers. Johnson sent another email to Puissant’s CEO on September 23, 2014 in which he attached a management representation letter and asked the CEO “can you copy this on to your letter head and sign and date April 12, 2014.”

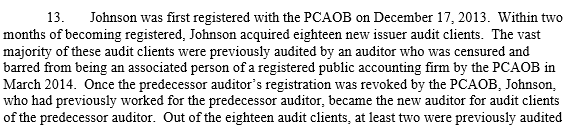

And:

An email dated September 17, 2014 from Primco’s CFO to its CEO states “…over the last 10 days we have been in Florida helping Terry [Johnson] with the pcaob review, one of the accounts picked was the […] primco file…so we have been working on this and several other accounts they want to see…unfortunately when the SEC calls everything else comes to a halt…”

As an added bonus, the CFO of Primco was Steven J. Corso, aka Stephen P. Corso, aka the guy who testified against the "Mafia Cops."

Some other fun things in the order include:

- "[A]n undated two sentence memo which stated 'Traveled to Wood Valley to observe existence of ranch. Attached find pictures of the farm as well as documents that were found online regarding the farm.' "

- "Johnson further failed to establish a materiality level for the 2012 year-end audits."

- "With the exception of audit clients, Boreal and Primco, Johnson did not meet any employee of the Eight Issuers or visit their offices."

- "Johnson acknowledged his audit failure in this area [SAS 99], testifying, 'Yeah, they [risk factors] were present. That [the SAS 99 audit planning & risk

assessment] should have been checked yes.' "

For all this bad auditing (which he actually didn't admit or deny), Mr. Johnson agreed to a suspension and to pay over $150k in disgorgement of fees and fines. The Order is as convoluted as it seems but I promise that you'll enjoy reading the whole thing.