Last month, the PCAOB released its 2011 inspection report for PwC. With a 41% deficiency rate for the 60 audits inspected, it's safe to assume that the firm wishes it could have put up a better number.

As we noted at the time, Papa Whiskey Charlie encouraged the PCAOB to step up its game a little so that firm can quit sucking so much (aka improve audit quality). But in the meantime, they outlined a number of steps it has taken to, yes, quit sucking so much (aka improve audit quality).

Here are the first items listed in the letter signed by Bob Moritz and Tim Ryan:

- Investing significant amounts of time and attention of Firm leadership in understanding, evaluating and implementing actions designed to support achievement of our quality initiatives

Sounds great, right? Well, a couple of months ago, we received a message from a PwC auditor who informed us that the firm had recently communicated an upcoming change to its policy of supervision and review for public company audits.

Here's the text of the new policy with some bolding to make it easy on you:

The following policy changes are effective for audits of periods ending after December 15, 2012:For public company audits […], a manager or partner is also required to perform a detailed review of work where the first level of review was performed by a senior associate. This requirement also applies to non-public company audits, except in lower risk audit areas identified by the engagement leader and evidenced in the approved Assigned Workflow Report.On public company audits […], the engagement leader should review documentation supporting our understanding of the "end-to-end" flow of transactions in business processes and our identification of likely sources of potential misstatement (LSPM), which is expected to be included in Gather Evidence view in multiple instances of the EGA entitled "Identify risks and understand controls in the business process – [business process or FSLI name]". The engagement leader should review, at a minimum, the flow of transactions documentation and completed LSPM templates for business processes related to revenue, inventory, business combinations, and impairments, and for those business processes that impact financial statement accounts that present elevated or significant risks of material misstatement.

1 – Does this new guidance requiring at least manager-level review on every workpaper improve audit quality? — No. If a senior first reviews a workpaper knowing that a manager is going to come behind them and review it again, their review is likely going to be lighter as a result while the manager reviews knowing that the senior has already reviewed it. This is also known as groupthink.2 – Are they [Ed. note: presumably, firm leadership] pushing for PwC to promote earlier? — The more managers we have to review these workpapers, the better, right? So why not promote people earlier so we can have more people that are eligible to review? This new guidance may drive title inflation more than anything.3 – If ever become a partner, I don't want to be reviewing the flowcharts and other templates that a first year put together. Last year, these weren't requirements. Now all of the sudden, it requires partner sign off? Seems like a typical knee jerk reaction from our firm.

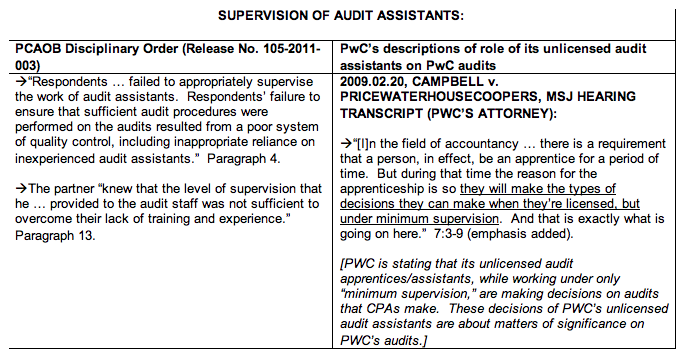

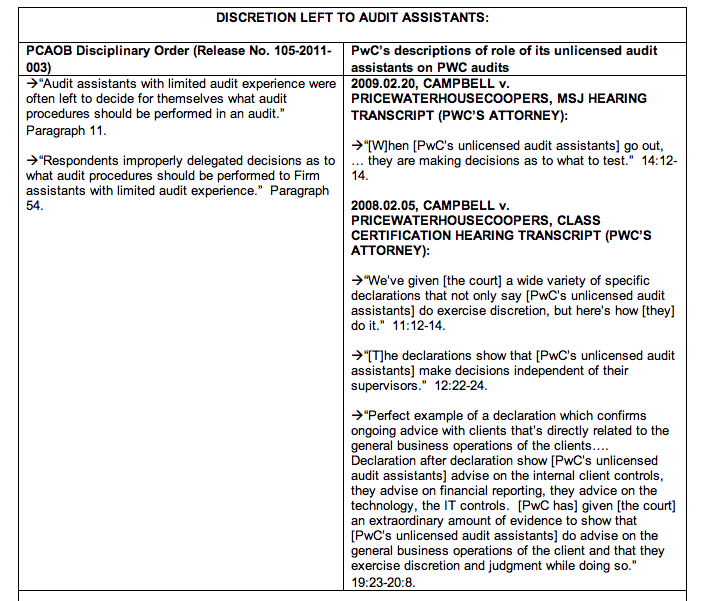

The firms have created a Hobson’s choice for the entry-level auditor. Their immediate superiors may ask them to do robotic, routine, data entry into pre-programmed audit software, scan hundreds of documents, or to ask questions of a senior client employee while using discretion and judgment in deciding if they’ve heard true and complete information. Either way, their choice is only to do what they’re told. During busy season they have been known to follow orders for 60-80 hours per week.

[W]hen audit firms expect entry-level professionals to, “exercise discretion and independent judgment with respect to matters of significance,” they are perpetuating performance requirements that contradict PCAOB Auditing Standards in service to avoiding overtime pay. More likely, the firms’ first objective is to perpetuate artificial status and value in the eyes of both college graduates and audit clients so the firms can continue to attract bright-eyed graduates and justify higher than necessary fees for work that is performed by the least experienced, but least costly, resources under general, or less than general, supervision by partners.

PCAOB spokeswoman Colleen Brennan declined to comment. PwC had no comment.

What now? Well, it'd be interesting to know if PwC's attorneys Campbell were aware of this new supervision and review policy. It'd also be interesting to know if the framers of this new policy were aware of what the lawyers in California were saying. And it'd also be interesting to know what the PCAOB thinks of the PwC's new policy and what they think of the arguments that PwC's attorneys are making in Campbell. We probably won't get direct answers to any of these questions, but it certainly reiterates the impunity and hubris of the large accounting firms and the PCAOB's inability to consistently enforce its standards. We're all getting used to it.