![]()

Listen to Oh My Fraud, a podcast by Caleb Newquist and Greg Kyte, and get free CPE through Earmark.

When accounting goes unaccounted for

![]()

Listen to Oh My Fraud, a podcast by Caleb Newquist and Greg Kyte, and get free CPE through Earmark.

Exposure Drafts appears every other Wednesday. Send your accounting cartoon ideas to editor@goingconcern.com. You can […]

Exposure Drafts appears every other Wednesday. Send suggestions to editor@goingconcern.com.

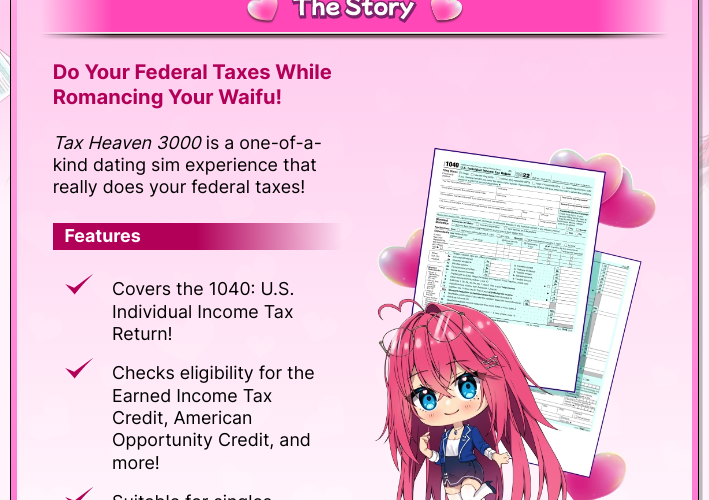

TW: TurboTax bashing Before you get all bent out of shape over an anime dating […]

Comments are closed.

Read interpretation 1.270.100 of the AICPA Code of Conduct. You don’t have to ask any close relatives whether they have a direct or materially indirect interest in any of your audit clients. Instead, it reads that should you “know or has reason to believe was material to the close relative or enabled the close relative to exercise significant influence over the attest client”.

BTW, the AICPA thinks you are nothing but a tool. Your hatchet job from 10 years ago created a lot of laughter. They were laughing at you.