Wow, we haven’t seen crazy unauthorized city spending like this since Rita Crundwell, except instead of horses it’s dogs and it’s like 1/30th of the spending because Washington, OK doesn’t have that Dixon, IL money.

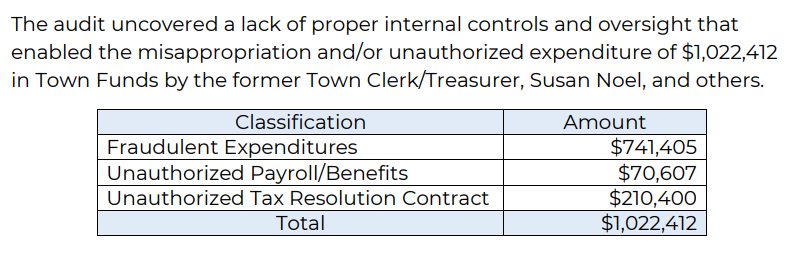

Oklahoma State Auditor & Inspector Cindy Byrd, CPA released a forensic audit report for the Town of Washington yesterday and for a town with 673 people they sure spent a lot. Well, her report alleges that more than $1 million of the approximately $3.3 million in expenditures from July 2020 to June 2024 was fraudulent. And boy did she bring receipts.

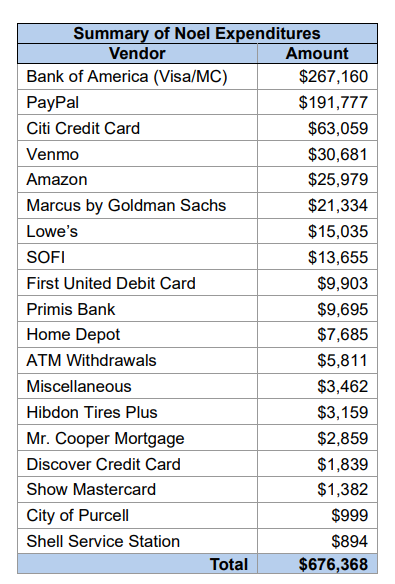

The report said it found that Susan Noel misappropriated $676,368 in Town funds. Town is capitalized in the report as in the town’s full government name Town of Washington so we’ll roll with that. There’s also the issue of people being paid more than they’re supposed to and as if that weren’t enough, from 2012 through 2019, Noel failed to submit payroll tax withholdings to the Internal Revenue Service (IRS), resulting in unpaid payroll taxes, interest, and penalties totaling $176,887.

“This is the worst example of board oversight I have seen in my 29 years of government auditing experience,” Auditor Cindy Byrd said in a press release [PDF]. “The Town of Washington is a small community with limited resources. From FY2021 to FY2024, roughly one-third of the Town’s total expenditures were either fraudulently misappropriated or spent without Board authorization. The responsibility for the financial welfare of the Town ultimately rests with the Board, which failed to exercise oversight of Town finances as required by law.”

You can tell she’s annoyed with the Board based on these several paragraphs in the report:

The issues addressed in this report show that the Town suffered major financial losses at the hands of its former employees. Although these losses are the responsibility of the alleged perpetrators, the Board also bears responsibility for failing to provide the oversight needed to protect public funds.

Several trustees asserted they were unaware of the unlawful expenditures, improper employee compensation, and poor oversight of revenue collections. Even though several of the questionable transactions appeared to have been purposefully hidden from the oversight of the Board, timely review of bank statements, check registers, or monthly expenditure reports would have revealed many of the questionable transactions. If those documents and records were not routinely presented to the Board, the Board had a duty to demand them and hold employees accountable.

However, it is important to note that not all trustees responded in the same manner. Trustee Joel Siria and former Trustees Duane Branham and Kara Cook raised concerns about the Town’s financial practices and sought access to the financial documents and records of the Town. Noel and Aday resisted in providing those documents.

In a small town, the lack of limited staff can make it difficult to separate financial duties. That makes strong Board oversight even more important. Although some trustees attempted to strengthen oversight, the Board as a governing body failed to provide the level of oversight needed to protect Town assets and is ultimately responsible for safeguarding the Town’s finances. The Board bears responsibility for the financial welfare of the Town.

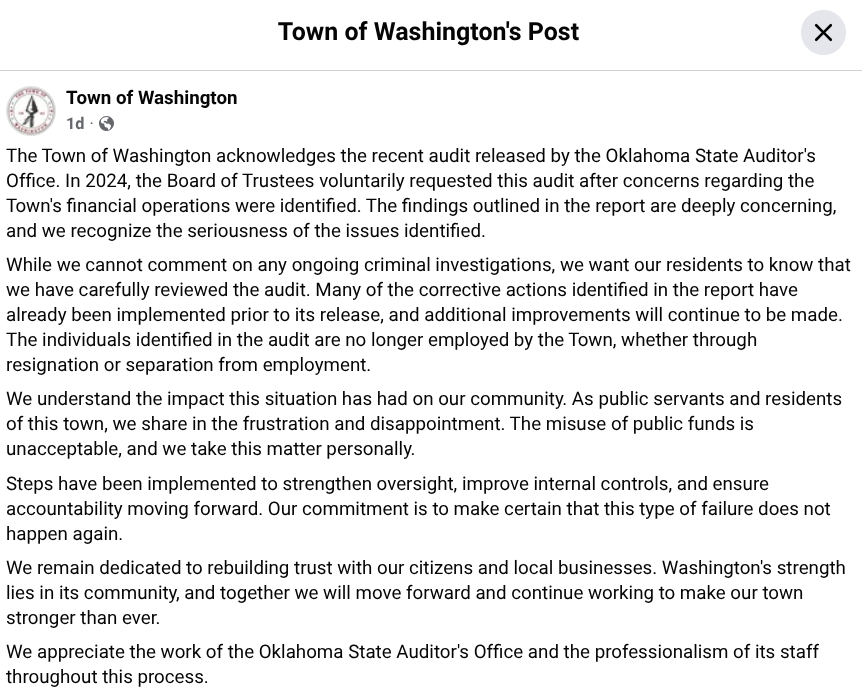

The Board responded on where else, Facebook:

We’ll embed the full forensic audit below but here are some highlights. First, the people involved were two longtime public servants who held the town purse:

The Town’s financial operations were primarily administered by the Town Clerk/Treasurer Susan Noel (Noel) and the Town Administrator Paul Aday (Aday). In their respective positions they exercised substantial control over the Town’s day-to-day operations. For most of the audit period, in addition to Noel and Aday, the Town employed a staff of four individuals: Noel’s daughter Kasey Lesher (K. Lesher) the utility billing clerk, Noel’s son-in-law T.R. Lesher the Town’s water operator and maintenance worker, and two police officers, Rubin Ruiz, Jr. and Larry Watts.

Bank records reflected that Noel and Aday were the sole signatories on the Town’s bank accounts from April 18, 2008, through July 18, 2024, the date Noel was terminated.

Noel served in her role as town clerk with financial oversight of the Town for approximately 17 years, from 2007 through July 2024, while Aday was employed by the Town for approximately 31 years, from 1993 through September 2024. The evidence established that Noel and Aday exercised extensive authority over Town finances.

The concentration of financial responsibilities among a small number of individuals, combined with extremely limited Board oversight created an environment in which unauthorized transactions and fraudulent expenditures occurred and remained undetected for an extended period.

And just like that, Town of Washington earned its place in a future Audit 101 textbook. The state auditor’s findings of poor internal controls are a given, it’s covered in depth around page 30-31 of the report.

Among the “Noel Expenditures” as they’re dubbed in the report are Bank of America credit card bills, almost $30,000 in Amazon purchases (which included a memory foam mattress, sectional sofa, coffee and espresso machine, a cordless vacuum cleaner, a vibration plate exercise machine, countertop ice maker, four-drawer file cabinet, and electric nail clippers for dogs), and $9,903 on the Town’s debit card for, among other things, a doodle puppy and puppy breeding rights.

Then there’s the $54,770 charged to the Town’s fuel fleet cards from January 2020 through July 2024 and $18,365 paid to local convenience store Sid’s Easy Shop from July 2020 to June 2024. Because the Town didn’t keep mileage logs or trip records, the state auditor was unable to determine the legitimacy of all these expenses. “Some fuel-related expenditures were problematic” due to their volume and frequency, the report said.

Full report is embedded below for your reading pleasure.

As global cash transactions have become increasingly complex, both the familiarity and training of accountants in the cash area may have actually declined. Most young adults no longer keep check books, and consequently, no longer perform the reconciliation process on their personal accounts. Instead, they simply check available balances either online or at an automatic teller machine, and adjust their spending habits accordingly. [

As global cash transactions have become increasingly complex, both the familiarity and training of accountants in the cash area may have actually declined. Most young adults no longer keep check books, and consequently, no longer perform the reconciliation process on their personal accounts. Instead, they simply check available balances either online or at an automatic teller machine, and adjust their spending habits accordingly. [